As we look at Tesla today, the situation mirrors late-2019: Tesla was about to open the Shanghai plant, which doubled capacity, and launch Model Y, which doubled the company’s total addressable market (TAM). When Tesla opens plants in Berlin and Austin, Tesla’s capacity will double again. The Model Y launch in Europe will double EU TAM (EU represents 20% of Tesla’s volume) and also puts Tesla vehicles closer to price parity with EU manufacturers, since there will be no import tax or shipping. We anticipate 2022 volume growth of 60%+ despite the fact the Cybertruck has been delayed until end of 2022.

In the US, the Biden administration’s US EV tax credit for eligible buyers is expected to be $7.5K-$10K and pass by late September. This will put Tesla at “EV credit parity” with other automobile manufacturers in the US, since currently, Tesla purchases don’t qualify for the EV credit as its $200K cumulative EV cap has been fulfilled.

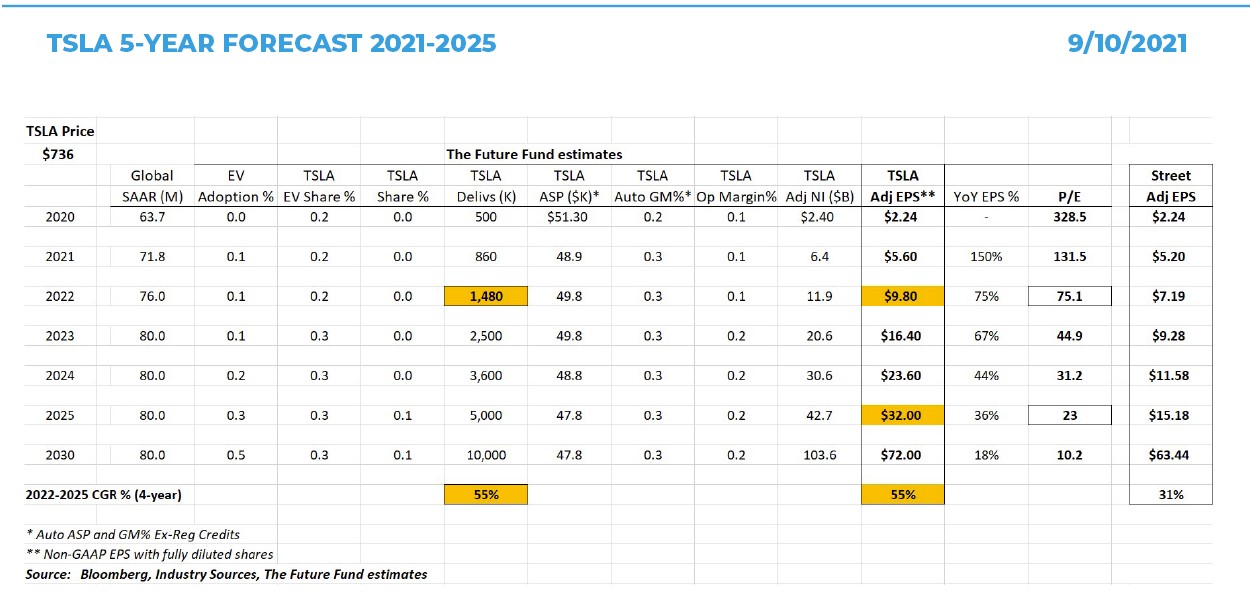

Earnings and Stock Price Estimates

In our opinion, Street volume and earnings estimates for Tesla for 2021 and 2022 are too low. We expect earnings per share (EPS) to come in around $5.60 for 2021 and $9.80 in 2022 vs. the Street estimates of $5.30 and $7.30 respectively. Once Berlin and Austin open, we expect Wall Street to boost its volume and EPS estimates for 2022 and beyond.

Over the next 6-12 months, our TSLA price target is $1,100, rising to $1,600 by 2025; this includes $0 for Robotaxi. In contrast, Ark Investment Management’s price target is $3,000 in 2025, which includes $1,500 for Robotaxis. We add no incremental value for Robotaxi (other than value from the $10K upfront cost as an option) because several US and Chinese competitors are already testing EVs with Level 4 autonomous driving capabilities while Tesla remains at Level 2. By 2025, we expect all automobile manufacturers to offer Level 4 autonomy, which would imply no incremental value for Robotaxi.

TSLA 5-YEAR FORECAST 2021-2025 9/10/2021

In our TSLA five-year summary forecast, we see volumes growing from 860K in 2021 to 5.0M in 2025, which has the potential to increase the company’s EPS from $5.60 in 2021 to $32 in 2025. At a 50x price to earnings ratio (P/E), which is consistent with 18-20% EPS growth 2025-2030, we estimate a $1,600 share price by 2025. Discounting this back at an 11.6% cost of equity (2% 10yr Treasury yield, 6% equity risk premium and a 1.6x beta = 11.6%) equates to a price target of $1,100.

Investment Controversy

Electronic vehicle (EV) adoption is surging globally — from 3% in 2020, to 5% in 2021, to an estimated 25% in 2025. That alone may drive 50% compounded Tesla volume growth between 2020-2025, assuming Tesla can hold EV share as EV adoption rises.

The Tesla investment controversy continues to be whether Tesla will lose EV share as internal combustion engine (ICE) competitors ramp up EV development efforts and reallocate $30B in advertising spending toward EVs. That’s been the debate for three years, and during that time Tesla’s EV share has grown from 17% in 2017 to 23% in 2020 and 24% YTD in 2021. What’s changed? Competitors are now poised to leverage the equities of best-selling branded products like the Ford F-150 and Porsche Macan and extend those brands into the EV space.

We also expect Tesla debt to be upgraded to investment grade after year-end, as Tesla’s cash and

free cash flow (FCF) overwhelm Tesla’s debt ($17.4B cash including Bitcoin vs. $7.6B debt. We forecast $4B FCF in the 2nd half of the year and $11B FCF in 2022). Many investors may miss the significance of Tesla being accorded an investment grade credit rating, which will reduce or eliminate the need for further equity raises as Tesla ramps up capacity between 2021 -2025.

The Opportunity

We expect Tesla stock to continue to move higher as fiscal year 2022 volume and earnings estimates are increased once the new Berlin and Austin facilities open in the fourth quarter. We believe investors are overestimating the negative impact of new EVs from competitors given Tesla’s expanding EV TAM as it launches Model Y to Europe, and as local EV production brings Tesla EV prices down closer to its European competitors. We believe the $7.5K-$10K US EV credit will act as a price cut for Tesla vs. others who already benefit from the current $7.5K EV credit. Finally, we believe investors are underestimating the 2023-2025 volume and earnings upsides as the Tesla Cybertruck and $25K Tesla subcompact launch globally.

About The Future Fund

The Future Fund LLC is an SEC-Registered Investment Advisor. We’ve identified 10 megatrends we believe are the most influential multi-year secular growth opportunities shaping the future. Our focus is on companies that can change the world by capitalizing on these fundamental changes in their markets.

Important Information

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Future Fund information may include statements concerning financial market trends and/or individual stocks, and are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such. The investment strategy and broad themes discussed herein may be inappropriate for investors depending on their specific investment objectives and financial situation. Information contained in the material has been obtained from sources believed to be reliable, but not guaranteed. You should note that the materials are provided “as is” without any express or implied warranties.

Past performance is not a guarantee of future results. All investments involve a degree of risk, including the risk of loss. No part of Future Fund’s materials may be reproduced in any form, or referred to in any other publication, without express written permission from Future Fund. Links to appearances and articles by Gary Black, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor’s investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment’s value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment’s value. Views represented are subject to change at the sole discretion of The Future Fund LLC. The Future Fund LLC does not undertake to advise you of any changes in the views expressed herein.

Future Fund, its clients and its related persons, including Mr. Black, hold financial interests in securities or issuers discussed in this material. However, any discussion of securities or issuers included in this material is not a recommendation to buy, sell or hold any particular security.

© Copyright 2021 The Future Fund LLC. All rights reserved.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS